- Moving the markets

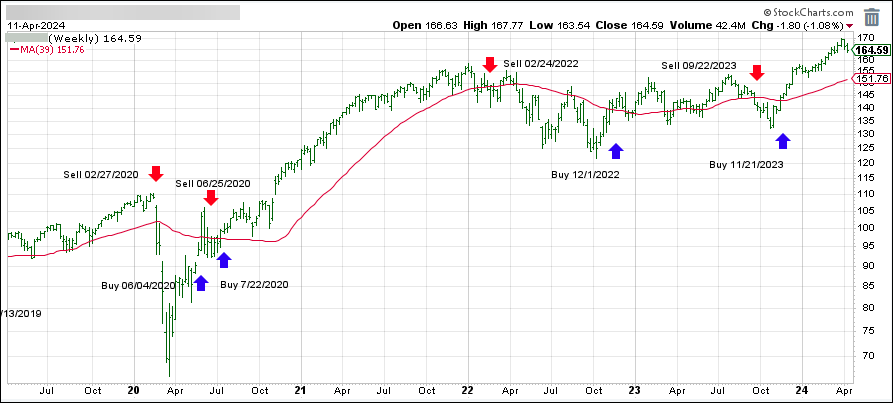

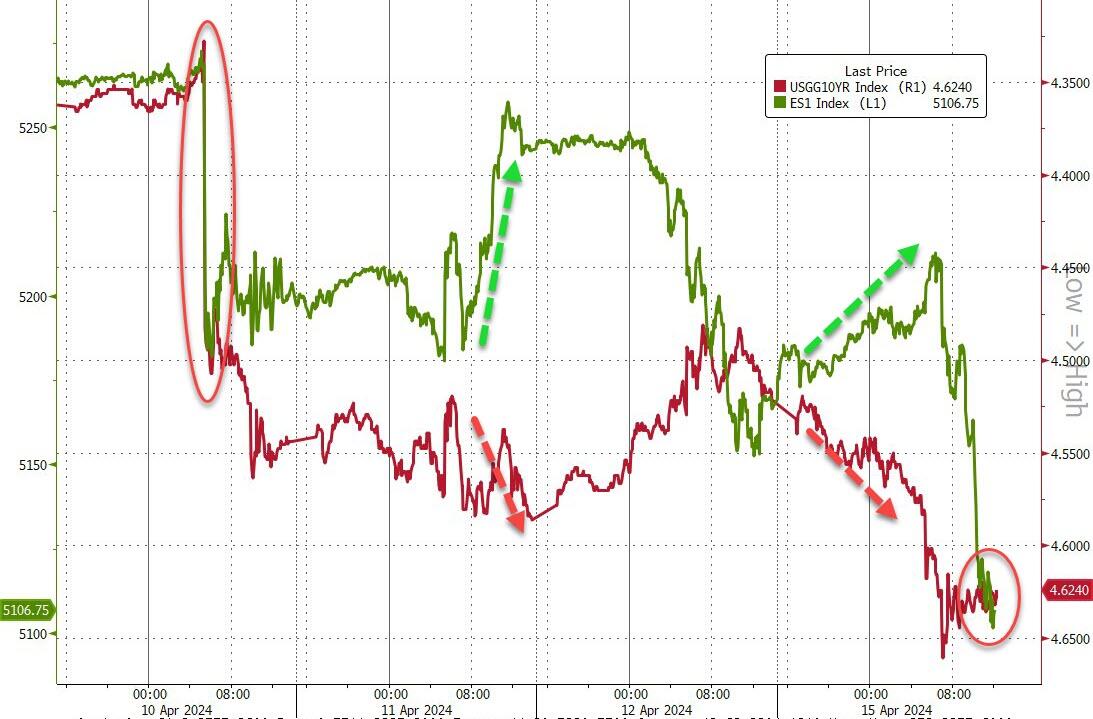

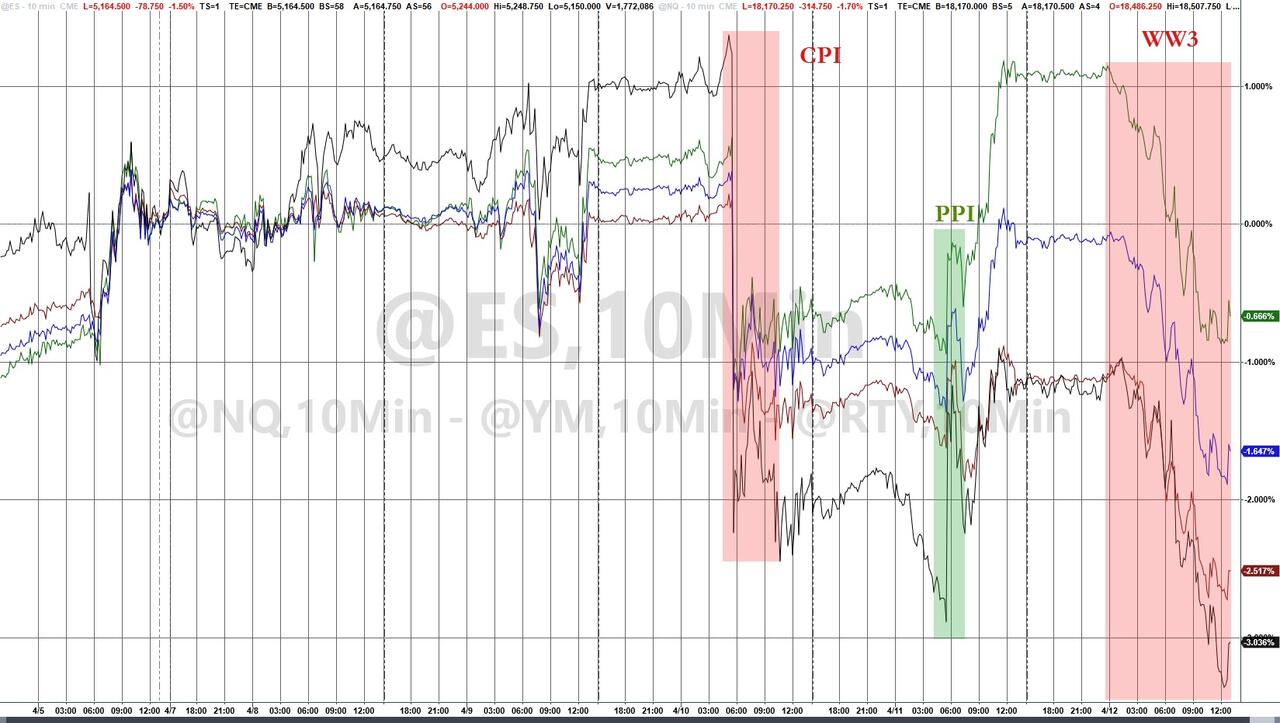

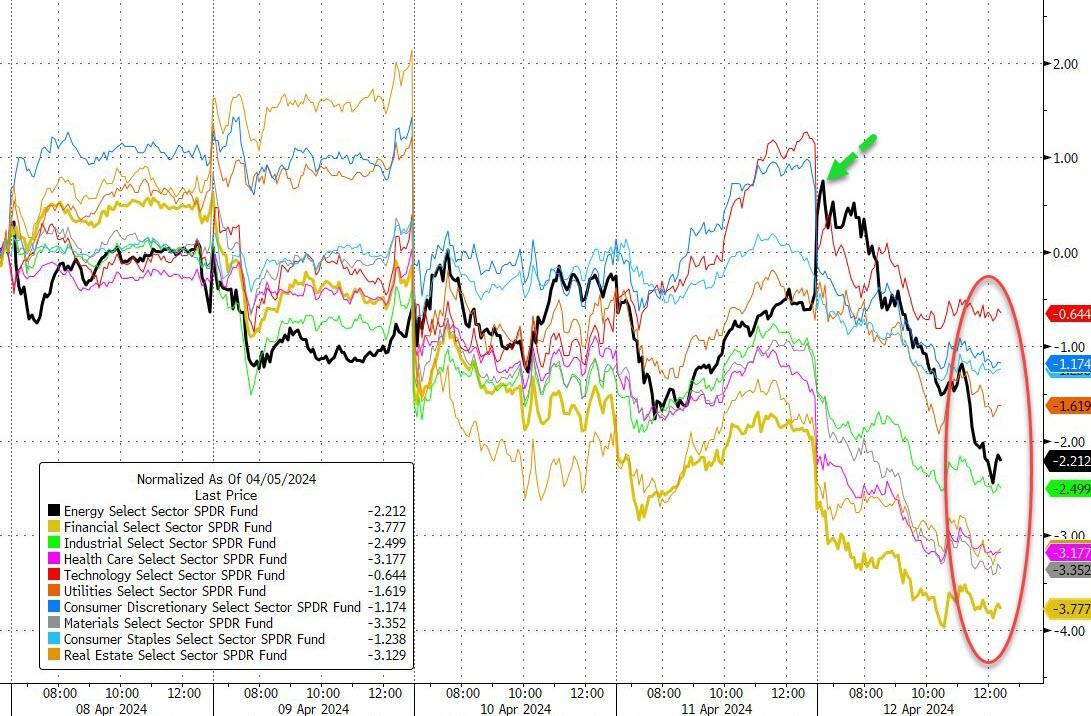

In today’s financial landscape, the S&P 500 experienced a downturn as investors juggled the latest corporate earnings with rising yield concerns and geopolitical tensions.

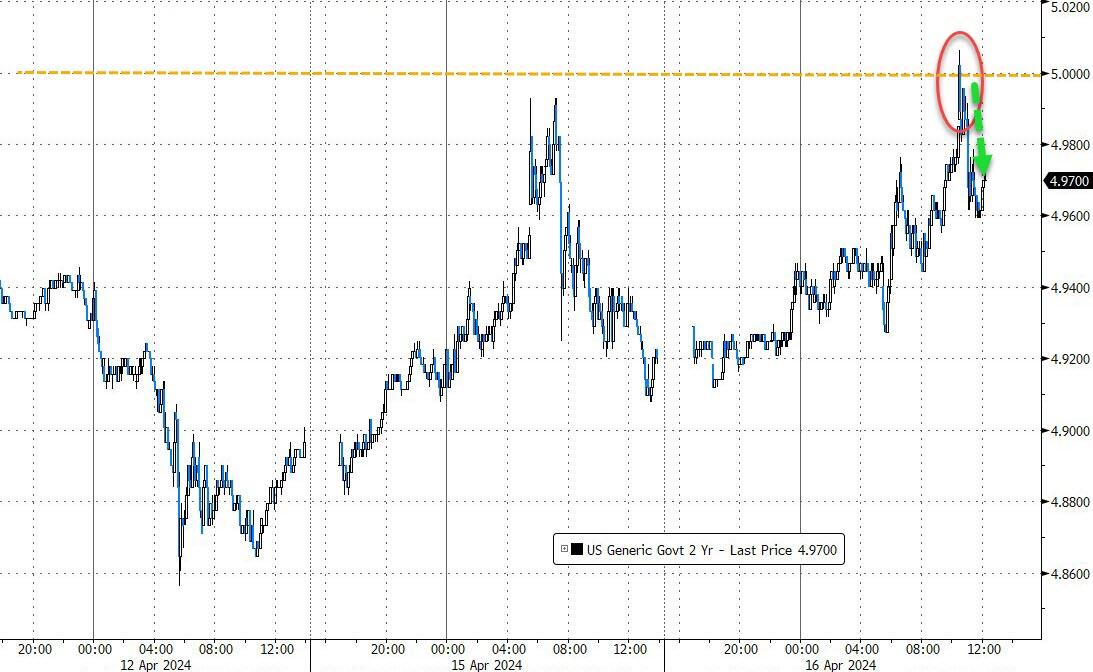

Federal Reserve Chair Powell’s remarks suggested that interest rates might remain high, dampening hopes for rate cuts and driving the 2-year yield above 5% for the first time since last November.

Despite the uncertainty, there’s a silver lining: most of the S&P 500 companies that have reported earnings so far have surpassed expectations, offering a glimmer of optimism. However, the persistence of higher interest rates has cast a shadow over this positive trend, with the 10-year U.S. Treasury yield soaring past the significant 4.6% threshold.

Globally, the market’s pulse quickened with news of Iran’s missile and drone strikes on Israel, contributing to a cautious sentiment. This unease was mirrored in the bond market, where yields surged, leading to a tumultuous day that saw the S&P 500 and Nasdaq close in the red.

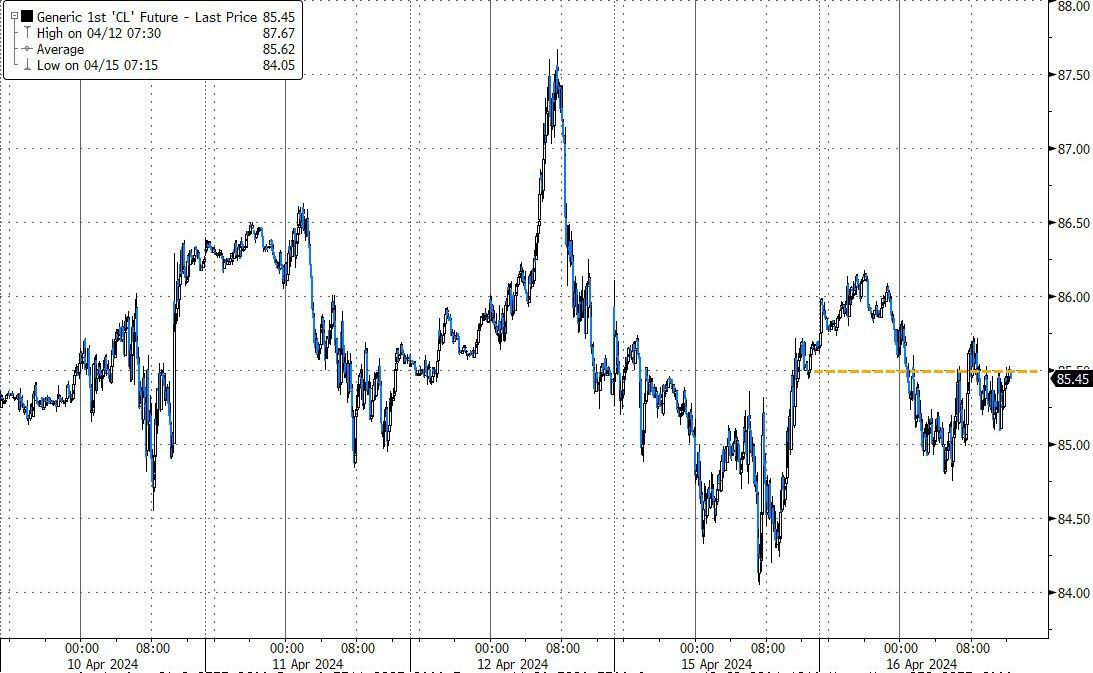

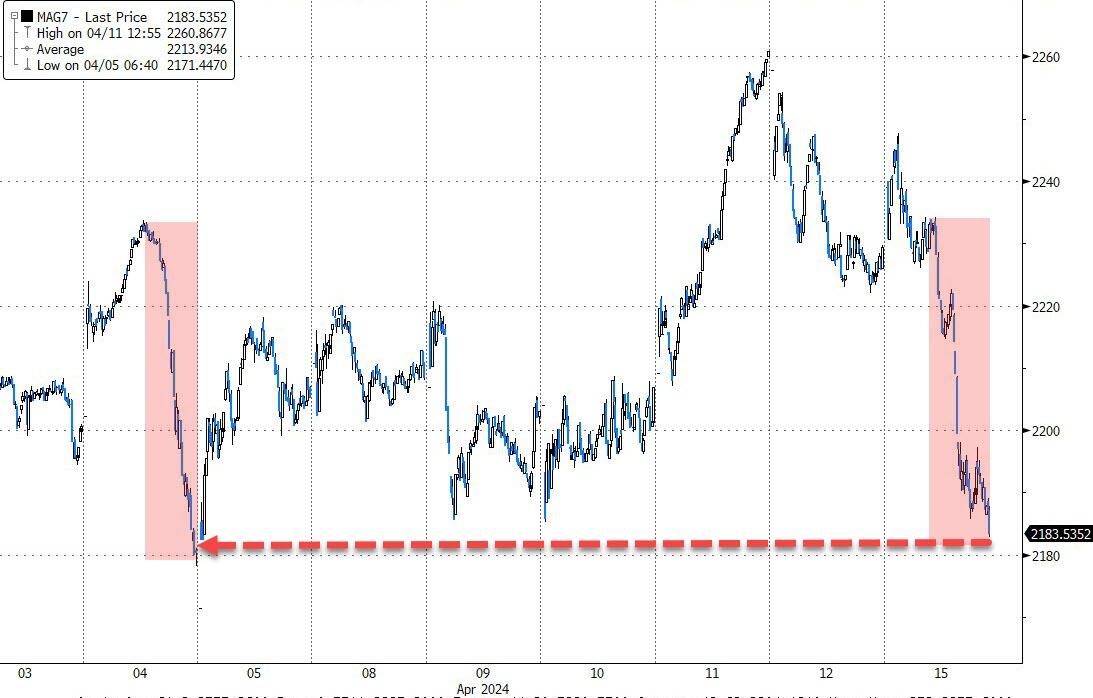

Amidst this, the MAG7 stocks remained steady, the dollar saw modest gains, while crude oil prices held steady, and gold reached a new record closing high.

As gasoline prices continue their upward trajectory, one can’t help but ponder:

Will the now half empty Strategic Petroleum Reserve be tapped once more to temper the rising fuel costs?

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}