|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

WEEKLY STATISTICS FOR OUR NO-LOAD MUTUAL FUND AND ETF INVESTMENT PLANS As of Thursday, August 23, 2007 By Ulli G. Niemann |

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

IN THIS ISSUE: 1. General Domestic

Equity Mutual Funds — BUY 2. Domestic Equity

Funds by Family — BUY 3. Exchange Traded

Funds Master List 4. Domestic Exchange

Traded Funds (ETFs) — BUY 5. International

Equity Mutual Funds/ETFs — SELL 6. Country ETFs

— SELECTIVE

BUY 7. Tax-Free

Investing — SELECTIVE BUY 8. Sector Fund

Investing (ETFs) — SELECTIVE

BUY 9. Sector Fund

Investing (Mutual Funds) — SELECTIVE

BUY 10. Bond &

Dividend paying ETFsNEW — SELECTIVE

BUY 11. On the Horizon:

Bear Market Funds — SELL 12. 401(k) Funds

(domestic) — BUY 13. New Subscriber

Info Weekly Market Comment: A decent

rebound last Wednesday moved our domestic TTI further away from a potential

Sell signal. However, the market looks shaky, and we may not be able to

ascertain true direction until the majority of the traders return to Wall

Street after Labor Day. As I

mentioned in my blog, we are holding our positions subject to our sell stop

rules. Are you interested in reading my

possibly politically incorrect ruminations about the market? I have

set up a blog, aptly named “The Wall Street Bully,” which will be updated

during the week. It gives you the opportunity to post comments and continue

the dialog. Take a look at it: http://thewallstreetbully.blogspot.com/ If you have

a newsreader, you can subscribe to it and new updates will be delivered to

you automatically. Alternatively, you can set this link up in your

‘Favorites’ folder and check at your convenience. This is a free service, so

please tell a couple of your friends. GLOSSARY OF TERMS USED: 1. 4Wk, 8Wk, 12Wk and YTD refer to

how these funds have performed or “appreciated” during these various time

periods. 2. %M/A (39-week Simple Moving

Average) shows how far above or below its long-term trend line a fund/ETF is currently positioned. 3. “Since 9/6/06” shows a fund’s

performance since that date. This date will be re-set once a new domestic Buy

Cycle starts. 4. DD% (DrawDown percentage) measures the drop from a fund’s

high to its current price during this Buy cycle (since is moving up given current given

economic conditions—which were favorable at the time. It is therefore in tune

with market momentum. Conversely, a fund with a large negative DD% number is a

lagging performer and should not be purchased at this time. 5. MaxDD%

(Maximum DrawDown percentage) is not

shown in these tables, but you will find me mention it quite frequently. If you were to go back to the beginning of the previous

Buy cycle ( trading day, and then select the worst (largest) DrawDown

number, you would have the information that I call MaxDD% (Maximum DrawDown Percentage). This allows me to look back at anytime and see which funds

have held up best and never hit our 7% sell stop. Those are the ones with a low MaxDD% (or low volatility)

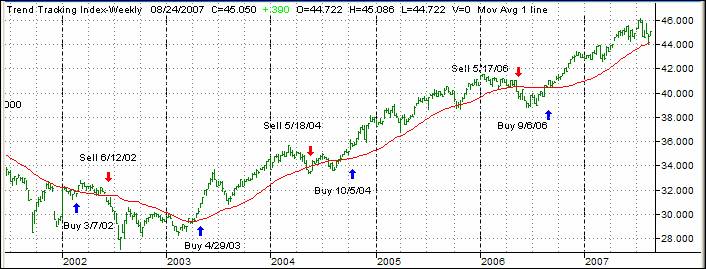

number and will be among my primary selections for the next Buy cycle. 1. DOMESTIC EQUITY MUTUAL FUNDS: BUY — since

Our

average portfolio (over $50k) has returned +24.81%, after management fees, for

the Buy Cycle (from Our

average portfolio (over $50k) has returned +8.10%, after management fees, for

the Buy Cycle (from Past

performance is not a guarantee of future results. Our Trend

Tracking Index (TTI) moved higher this week (green line in above chart) and

now remains above its long term trend line (red) by +2.22%. My sell

rules are as follows: I will liquidate any of my holdings if they drop by

more than 7% from their highs since I bought them, or if the TTI breaks below

its long-term tend line — whichever occurs first.

The link

below shows the top 100 domestic funds (out of 674) and is sorted by 4Wk

performance. Prices in all linked tables are updated through 8/23/2007,

unless otherwise noted. Price data not yet available at publication is

indicated with 00.00% or -100.00%. Please note, that I only track

no-load, no transaction fee or ‘load waived’ funds, which are available to me

through my custodian Charles Schwab & Co. Since all brokers and custodians

have different policies you need to check with yours first, before placing

any trades, as to no load availability and any charges or fees involved. I have identified those

funds, which are available to me as “load waived” funds or “advisor only” funds,

with an asterisk before their names. While this may not apply to all

brokerage firms, it should allow you to quickly locate those which are truly

no load.

http://www.successful-investment.com/SSTables/DomFundsTop100_082307.pdf TIP: Don’t forget to check the 401k

funds in section 6 as well, since many of them are available for all types of

investment accounts at different brokerage houses. 2. DOMESTIC FUNDS BY FAMILY:

American Century, Fidelity, Vanguard, ProFunds,

Rydex, T. Rowe Price — BUY http://www.successful-investment.com/SSTables/DomFFs082307.pdf 3. EXCHANGE TRADED FUNDS MASTER

LIST As per

request, I have added this ETF Master list so that you can quickly compare

various ETFs without having to reference other tables. The ETFs listed in the

table (498) consist of the following orientations: Domestic, International,

Country, Sector and Specialty. Momentum figures for all ETFs are not adjusted

for dividends. Please

note that I have moved all bear market ETFs to section 11, where they are

listed alongside the bear market mutual funds. http://www.successful-investment.com/SSTables/ETFMaster082307.pdf 4. DOMESTIC EXCHANGE TRADED FUNDS

(ETFs): BUY ETFs are

an excellent alternative to No Load Mutual Funds. They are a valid choice to

high mutual fund management fees, restrictive trading and redemption charges,

which have been a problem for years. If you’re

not sure how to use ETFs please read my FREE article about their pros and

cons, which you may view anytime at: http://www.successful-investment.com/articles24.htm All the

same Buy and Sell rules apply for domestic ETFs as they do for domestic equity mutual funds in

section 1. http://www.successful-investment.com/SSTables/DomETFs082307.pdf 5. INTERNATIONAL EQUITY MUTUAL

FUNDS/ETFs: SELL — Last Cycle from 8/17/2006 to 8/16/2007

The

International Index (green) finally broke below its long-term trend line

(red) on 8/15/07 and effective 8/16/07, we liquidated our last remaining position

and will remain on the sidelines in money market for the time being. This

cycle lasted exactly one year and started on 8/17/06 after the devastating

losses of May and June of that year. Time will tell if the domestic market

will follow the internationals to the downside as it did last year to the

upside. As of

today, the International Index has broken above its trend line by +0.85%. I

will continue to watch prices action to be sure that any recovery can be

sustained before making any new commitments. The

listings in the link below represent some of my choices of the international

funds I track. Please note that I have added Vanguard, Fidelity, T. Rowe

Price, Rydex/ProFunds and American Century funds.

They are sorted by 4wk performance: http://www.successful-investment.com/SSTables/InternFunds082307.pdf Be

advised that many international funds may not be available to you since they

carry a load. However, while I am able to purchase these for my managed

account clients as ‘load waived’ funds, this doesn’t help you much, if you do

your own investing. This is why I have included some appropriate ETFs in the

above list. 6. COUNTRY ETFs: SELECTIVE BUY While I

believe that the This

addition to my newsletter will allow us to also invest selectively in

countries with better performing stock markets. With the proliferation of

ETFs over the past years, we are now able to invest in a variety of countries

using low cost index ETFs. The chart

shows the Austria Index as an example:

The link

contains a list of 39 countries/regions, which I am tracking weekly. Please

note that the data in this table do not include adjustments due to

distributions. http://www.successful-investment.com/SSTables/CountryETFs082307.pdf As you

just witnessed during May and June 2006, country funds can be volatile and

the use of a trailing stop loss (I use 10%) is imperative to protect your

portfolio from severe downside moves. 7. TAX-FREE INVESTING This

section shows some of the Closed End Exchange Traded Bond Funds (CEETBFs) as

discussed in my free e-Book “How to

Earn 5% - 6.5% Tax-Free Income,” which can be downloaded from my site. This new

addition to the StatSheet is a managed account service I offer. Choosing the

right CEETBF out of over 500 takes a lot of work, and special knowledge is

required to customize a selection of funds specifically suited to your needs.

To

identify the general trend of these funds, I have created the TFI-Index, as

illustrated in the chart below. If the Index (green line) is above its

long-term trend line (red), we are in an environment of lower interest rates.

If it breaks below it, we are seeing interest rates rising.

The table

below is a small sampling of what is available. Be advised that the columns

“Discount,” “Current Dividend Yield,” and “YTD” are updated weekly so that

you can see and track the impact changes in interest rates are having. The

data is as of 8/22/2007:

Please

note that many of these funds have been around for a long time and therefore 10-yr

annualized returns are available for most of them. All of them are exempt from Federal taxation and,

depending on what state you live in, maybe exempt from State taxation as

well. Here’s

the glossary of terms used: 1. 1 Yr

Return*: The return over the last 12 months consisting of appreciation and

reinvested dividends. 2. Since

Inception*: The annualized return since the fund started operating. 3. 10 Yr

Annualized Return*: The annualized return over the past 10 years. 4.

Discount from NAV: The discount or premium from Net Asset Value (NAV) this

fund can be currently purchased for. 5.

Average Credit Rating: A key number which shows the quality of the fund with

AAA being the highest. The percentage shows how much of the funds holdings,

as a percentage, are in AAA rated bonds. 6.

Morningstar (MS): The current Morningstar rating. NR means that it is not yet

rated. 7.

Current Div. Yield: That’s the income being generated and it is paid out on a

monthly basis, if you wish. This represents spendable

income. 8. YTD:

Shows the Year-To-Date performance (without dividends) to demonstrate the

effect of changes in interest rates. Some funds are showing capital gains,

other capital losses. This is a very short-term view. These types of

investments should only be made with at least a 5-year time horizon. There are

many other factors, which come into play, when evaluating CEETBFs. This

section is only designed as an introduction. If you do your own investing in

this area, be sure to read my new article titled “The 10 Rules of Successful Tax-Free Income Investing,” which is

posted at: http://www.successful-investment.com/articles31.htm If you have

a need to generate reliable monthly income, please call me, or go the

following link and submit your request: http://www.successful-investment.com/TFI *As of 8. SECTOR FUND INVESTING (ETFs): SELECTIVE BUY To

diversify our portfolios, we always need to look for different opportunities

to invest our money. The table of sector fund listings (ETFs) in the

following link covers a broad spectrum of possibilities. The sorting order is

by 4Wk performance: http://www.successful-investment.com/SSTables/SectorETFs082307.pdf I

personally invest no more than 5% of portfolio value in any one sector and use

a 10% trailing stop loss to minimize the risk. I have taken several positions

and will add more if market momentum keeps improving. 9. SECTOR FUND INVESTING (Mutual

Funds): SELECTIVE BUY If you

prefer using Fidelity’s wide variety of excellent sector funds, you will like

this new addition. Here as well, sectors can be volatile, and I advise the

use of a sell stop just as we do with ETFs. The

sorting order is by 4Wk performance: http://www.successful-investment.com/SSTables/SectorMFs082307.pdf 10. BOND & DIVIDEND ETFsNEW: SELECTIVE

BUY If you

prefer using ETFs for the generation of income, here’s a list of bond and

dividend paying ETFs. It’s important to first look at how theses instruments

have held up in terms of momentum figures. Then you should visit your

favorite financial web site to examine yield and other details. http://www.successful-investment.com/SSTables/Bond_DivETFs082307.pdf 11. ON THE HORIZON: Bear Market

Funds: SELL

The above

indicator represents our Short Fund Composite (SFC) to be used as a trend

indicator for Bear Market Funds. After having

stayed above its long-term trend line during the correction of May/June 06,

the SFC has now broken below it by -1.71%. I will not take any positions

until our TTI (section 1) breaks ‘below’ its trend line and the SFC breaks

‘above’ its trend line, which would confirm bearish tendencies, before I

consider committing to this market. Below are

the most commonly available bear market funds and their momentum figures: http://www.successful-investment.com/SSTables/BearFunds082307.pdf Please

note that some of the above funds try to outperform the index they are tied

to by the percentage stated. While this can enhance your returns it can

certainly accelerate your losses as well. Personally, I prefer the

conservative route and, therefore, I will not use the leverage available. 12. 401(k) Funds (domestic): BUY The list

(featured in the link below) displays commonly held 401(k) domestic equity mutual funds showing

their latest momentum figures to go along with the Buy and Sell signals of

the TTI in section 1. The same stop loss rules apply here as well. Since

fund choices are limited in any 401k plan, be sure to roll your assets into

an IRA if you leave your job. Let me know if you need help with that. In the

meantime, however, you can benefit greatly by at least not buying the worst

fund at the wrong time. If you follow our plan, you will never again buy one

of those highly volatile sector funds, when you really should be out of the

market altogether. Since

this list has grown quite a bit, I have sorted it now by Ticker Symbol in

alphabetical order. This should make it easier for you to locate those funds

you are tracking: http://www.successful-investment.com/SSTables/401k082307.pdf 13. New Subscriber Information To get you a head start on more

successful investing, please click on: http://www.successful-investment.com/newsletter/How_to_use.pdf and download our “How to use” information sheet and

last year’s “Buy Signal”

information: http://www.successful-investment.com/weekly/BuySignal042803.pdf Also, my daily blog posts at http://thewallstreetbully.blogspot.com/

should help you to become more familiar with my approach. If you

still need some guidance, feel free to contact me. Special Notes: 1. I have

taken great care in selecting only mutual funds with no loads and no

redemption fees. However, policies vary from one brokerage house to another.

Before placing any trade, make sure to verify with your broker or custodian

as to any charges and fees involved. 2. Be

aware that, because of the mutual fund scandals, some fund families have

added early redemption fees. While some are reasonable (30 days), others are

ridiculous by trying to tie up the individual investor for 180 days, or

you’re being charged a 2% fee to opt out early. Be sure to check first before

placing any order. 3. Should

there be a sudden change in investment positions, I will send out a special

e-mail bulletin immediately. 4. I will

limit the tracking of 401k funds to only the first 150 submitted to me. If you

are interested in having your portfolio professionally managed using our

methodology, feel free to contact me directly or visit our website http://www.successful-investment.com/money_management.htm

for more information. My e-mail

is ulli@successful-investment.com

and my phone is 714.841.5804 Until

next week. Ulli… ========================= Ulli G. Niemann Registered Investment Advisor 714.841.5804 =========================

DISCLAIMER (c) Copyright Successful-Investment.com,

2003. All rights reserved. No portion of the above message may be

republished, retransmitted or forwarded without our express written consent.

Violation of this copyright may result in service cancellation. Use and/or

reliance on this service are strictly at the subscriber's own risk.

Subscriber must maintain compliance with our Terms and Conditions. We will

not be liable for the acts or omissions of any third party with regards to

delay or non-delivery of the 'Successful-Investment' notification. We shall

not be liable for incidental, indirect, special or consequential damages or

for lost profits, savings or revenues of any kind, whether or not we have

been advised of the possibility for such damages. Ulli G. Niemann is a registered investment

advisor pursuant to the California Department of Corporations. The

information presented herein is for informational purposes only and does not

constitute an offer to sell securities or investment advisory services. Such

an offer can only be made in those states we have established a

"notice-filing" status or where an exemption from notification is

currently available under the de minimis exemption rule. The investment advisor is an independent

advisor and receives no compensation from any corporations, brokerage houses,

organizations or special interest groups by making recommendations to

purchase any of the investment products used. The advisor is a fee-only

advisor and receives no commissions for client trades. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||